http://www.eeherald.com/section/news/onws201408001.htmlLet's talk briefly about where the chips are coming from, the general rankings and who is growing and who is not growing right now ....

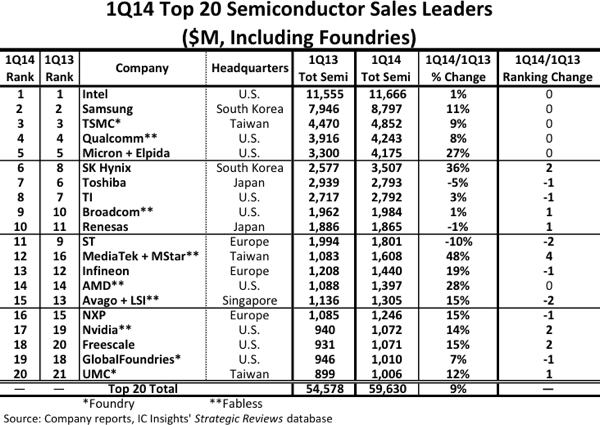

This is from the first quarter of this year, showing the traditional order of ranking that has been sitting around for the last 4-5 years basically unchanged. What is changing is the volumes this ranking order is based upon (note: instead of being twice as big or bigger, Intel is only slightly bigger than Samsung right now).

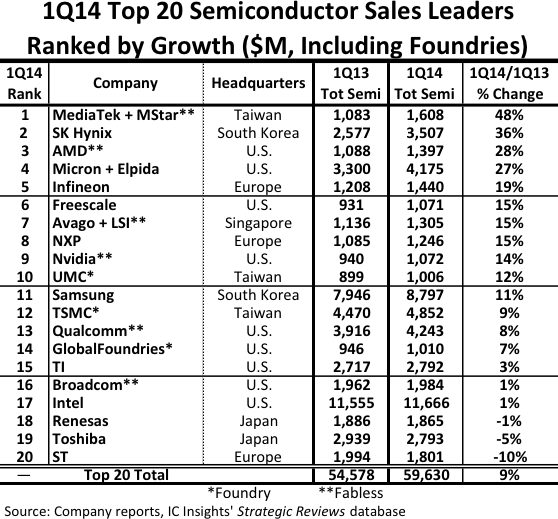

So, let's look at who is growing (or not as the case may be)

Intel has not ever been considered as a fab for hire before this year

Intel has not ever been considered as a fab for hire before this year, so their fab ranking history is very very sketchy right now.

Most all of their dollar based ranking data is skewed, because they would only report their production

at full retail value.

Intel chips are never sold at retail value, ever.

A fab has to report the real sales price for the chips it produced x number of chips produced, and Intel refuses to do this.

Complicating this issue is the fact Intel has been selling all of its low end chips at a strong loss (sometimes at over a 100% loss) while trying to break into mobile.

(as in sell it

at a strong loss, but report it at retail price as a + number ???)

Also complicating Intel's reporting is that their fabs are currently only partially utilized right now but Intel chooses not to tell anyone just how low this partial utilization level has gone.

The last factual reporting done by anyone based upon real known raw output numbers ranked Intel in the #7 position of all fabs based upon the output of finished chips.

TSMC was the largest chipmaker in that "real output" list by a considerable margin. And yet Intel claims to be 3 times bigger than TSMC by using full retail pricing for all products and reporting their "overall size" off of maximum theoretical capacity (while actually running at less than half of that right now due to low demand).

Intel is fixing this by shutting down some offshore fab plants, just not quickly enough to keep up with the drop in demand for their products.

So, Intel is now trying to peddle new 14nm lithography technologies that they are claiming are "production ready". So far they have sold this production capacity once already this year to Altera then defaulted on this deal earlier this year by not being able to meet either the production start date nor to get close to the predicted cost to produce the Altera 14nm chipsets. Altera went back to Samsung and their 20nm process for what they needed.

As a fab for hire, Intel is racking up a very spotty history in their new fab for hire endeavor.

What is clear to all parties is that Intel's interior pricing structure is way way way out of line with the rest of the fab industry -- as are every volume or costing based or structure based number that they have been using to create their internal "Intel Success" numbers that they have been using for years and years with their stockholders.

It would be very hard to buy any large scale 14nm production commitment out of Intel right now because it is clear the people negotiating with you have no choice but to actually use these sorts of funny Intel internal numbers to base their offers to you .... and once harsh reality peels the layers of vapor and fudge off that actual real production run of chipsets they will cost you more and it will come to you slower than initially offered.

It would be hard to buy Intel stock right now, knowing that the numbers reported to shareholders are "unique" to Intel in both structure and source.

"Vapor" and "fudge" is not how a fab for hire (or any other business) operates -- brutal, total honesty is how a fab for hire operates. Intel doesn't get this yet.

Look to see Intel's final 2014 rankings decline still further as the vapor fog bank is replaced by some slightly more honest fab-style reporting. Also look for the next Intel management change to come about sometimes fairly soon as the stockholders are pissed off at being lied to. This sea change in management will likely be part of a major restructuring of the company similar to what MS just went through. There will be some large restucturing charge offs to cover some past sins that need to be properly buried at last.

Intel's current predicted growth of 1% is also a made up number -- actually Intel is still shrinking at the same rate as classic PC is shrinking (around -6 % year on year so far). Intel has been hiding this in their utilization numbers up until this point but running any plant way below maximum capacity is VERY inefficient and costs the company yet more money that has to out somewhere at some point in time.

Intel cannot continue to claim "1% growth" off of their current attempts at loss leader mobile chip production as they have LOST MONEY (billions and billions) to produce these chipsets.

Losing money is not "growth" -- just ask your accountant, he will tell you. Report your stuff monthly at full retail value and producing it inefficiently due to poor plant utilization and

selling it at a strong loss because you just plain have to must be reported eventually as an additional "adjustments to revenue" or a massive "restructuring" loss.

Rolling it and hiding it from one quarter to the next is illegal and will cost the upper level dudes their jobs.

One wonders what Intel really really looks like right now, once you peel off the onion layers of vapor this and fudged that .....

Dorothy, don't pull back that curtain, honey -- you won't like what you see. And put your emerald glasses back on, sweetie -- let's try to be good little Intel stockholders, OK ??

Dorothy, don't pull back that curtain, honey -- you won't like what you see. And put your emerald glasses back on, sweetie -- let's try to be good little Intel stockholders, OK ??

Aw, gee wiz -- I warned you ......

The Great and Powerful OZ is really just a flim-flam sham of a man, a old short fat bald headed little man sitting on a tall tall stool just so he can reach the levers that control the big flames and smoke generators actively wreathing the puppet head out there on the stage.  Hey !!! Can you please stop it with all the hollering, explosions, shooting flames and billowing smoke for just a minute -- this isn't fun sitting out here getting roasted .....

Hey !!! Can you please stop it with all the hollering, explosions, shooting flames and billowing smoke for just a minute -- this isn't fun sitting out here getting roasted .....

Pages: 1

Pages: 1